[The following email from Dan Carson was shared with the Davisite for posting]

Dear City Council and Fiscal Commissioners:

Attached please find a city staff report authored by the City Manager and the Finance Department — dated May 19, 2026 and titled “Fiscal Year 2026/27 Mid-Cycle Budget Update” — that was recently provided to you for public hearings this week. Given the brief timeline available for public consideration of this report by the Council and the Commission, I am sharing these comments with you in the interests of ensuring that you obtain critical information needed to assess the proposed actions and their potential effect on our city’s fiscal stability and integrity.

As you know, I served as a fiscal advisor to the California Legislature for 17 years, concluding my state career as Deputy Legislative Analyst of the nonpartisan and independent Legislative Analyst’s Office before serving for nine years on the City of Davis Finance and Budget Commission and then the City Council.

In summary, my analyses indicates that the first steps to address the city’s budget shortfalls being proposed by city management are reasonable but will fall far short of what is needed to address a severe funding gap caused primarily by dramatic and excessive increases in employee pay and benefits approved by the Council in a series of recent multi-year labor contracts. The budget package also does not provide the level of funding needed to fix our roads and bike paths and other infrastructure and discloses that it “defers” more capital improvement projects it does not identify. I recommend the Commission and the Council take a series of actions described below to address these issues.

1. Plan Includes Reasonable First Steps to Contain City Costs…

The city’s proposed new budget package contains some significant and justifiable actions to address the city’s budget problems, and promises that there will be more actions to come. The proposed $1.4 million in proposed budget reductions would reduce General Fund spending in 2026-27 by a net amount of $600,000 or 0.6 percent, after accounting for a series of budgetary increases that offset these savings. The list of budget reduction proposals include the elimination or consolidation of a few staff positions, at least some of them vacant; shelving some purchases of equipment and office supplies; and substituting state grant funds for General Fund support of the city respite center.

The Commission and Council should ask city staff for more detailed information about these proposals to verify that they are consistent with prior Commission recommendations and prior Council decisions and policy priorities. However, in general, these actions appear to be reasonable and likely would achieve the level of savings identified, while having little if any impact on the availability or quality of services provided to city residents. Thus, they generally warrant serious consideration and support.

2. …But The Budget Package Before You Is Far Short of What’s Needed

As the staff report itself clearly and repeatedly acknowledges, the new budget proposal on your agendas this week falls far short of addressing the funding gap identified in the city’s 2025 long-term General Fund fiscal forecast. That forecast predicted that the city’s General Fund reserve, which under city policy is supposed to be 15 percent, could dangerously erode to zero within the next few years because of a persistent and ongoing multi-million dollar structural deficit. The proposals now on the table could delay, but would not end that threat.

City staff is promising that more proposed solutions are coming. The staff report indicates that some additional budget actions, described as “further recommendations and refinements to the proposed budget,” will be presented to council on June 2. City managers also say that “the City Manager is developing a larger reorganization plan in anticipation of upcoming retirements that he will present to the City Council in February 2027” that “will address the remaining General Fund expenditure gap.” The report further states on page 06-2 that these additional unseen proposals will “close the General Fund gap completely,” although it does not specify when in the future that this feat would be accomplished.

The underwhelming nature of the budget package placed on Council and Commission agendas this week is surprising, given earlier and oft-repeated public assertions over the last year that city leadership would roll up their sleeves and adopt tough new budgetary changes to solve the city’s budget problems now. The new staff report is silent about what further budget actions are contemplated and which city services, programs, and/or staffing would be affected by the additional budget solutions that are to be released on June 2 and sometime in February. Tough actions may indeed be coming, but if that is true, we have no idea what they are and when they would take effect. Notably, the “reorganization” proposal would be released in February and, with only four or five months left in the fiscal year, it would likely produce only a fraction of the savings needed to help address the city’s structural deficit in 2026-27. The city may once again find itself putting off any difficult budget-balancing decisions until sometime next year.

The Council and the Fiscal Commission should ask city staff to provide additional information about the additional proposals for budgetary actions that are due on June 2 and in February. That additional understanding of these unseen proposals is needed if you are going to meaningfully evaluate whether the city staff’s approach provides a realistic pathway for addressing the city’s General Fund structural deficit in a timely way and before the General Fund reserve erodes to an unsafe level. Also, the Council or the Commission should not be afraid to put their own proposals on the table now to address the city’s serious funding gap. More solutions are needed because addressing the immediate shortfall in funding for General Fund operations is only part of the problem. As discussed below, even if that problem were fixed, that would still leave a huge gap in the funding needed to fix deteriorating city infrastructure.

3. Budget Efforts to Fix Infrastructure Are Lacking

The May 19 budget report is not clear about the total amount of funding that is proposed to be committed from various funding sources, including the General Fund, to maintain our city’s roads and bike paths. Page 06-2 of the budget report calls out that $3 million will be provided from the General Fund for maintaining our streets and roads. However, that number represents the minimum level of funding that must be provided by the city to qualify for certain state gas tax funds. The new report does not explain the total resources from all funding sources that would be allocated to pavement maintenance in 2026-27 under the revised city budget. It does not explain how the level of funding for the pavement maintenance program would change from 2025-26. Notably, no changes in the level of General Fund or other fund sources for pavement work are identified in the list of budget amendments presented for council approval on pages 06-12 through 06-15. This is noteworthy because the current level of funding is insufficient to keep pace with city needs. An official report released last year by the city’s pavement maintenance consultant documented that, absent an immediate and ongoing commitment of an additional $3 million in annual city funding for such projects, the backlog of roadwork alone will grow by about $50 million over the next ten years.

The budget package now before the Council and the Commission lacks many details, such as the budget worksheets outlining the expenditures of each Capital Improvement Project and the timing and source of funding for each individual project. Based on my reading of the information in the May 19 budget report, the 2026-27 budget package would not address the lack of city General Fund support for the maintenance of parks, traffic lights, and other critical city facilities. Moreover, the new budget report states on page 06-2 that the city is now “deferring timing of several capital projects” it does not identify. If more grant-funded projects are among those being delayed, the consequences of such a budget action could be serious. The city’s financial inability in recent years to provide promised matching funds for projects like the Richards overpass could ultimately result in the loss of those grant funds, if that in fact has not already occurred in some cases.

Accordingly, you should request an update on the city’s Capital Improvement Program. That update should include (a) a table summarizing all current budget items related to maintaining streets and roads and bike paths and their funding levels by funding source for prior years, 2026-27, and subsequent years, and any changes to those funding levels that are now being proposed as part of the staff’s May 19 budget report; (b) a list of the capital projects that are being deferred, along with their proposed funding source and amount of budget savings; (c) an update on the status of other city projects that have been frozen in the last couple years because of budget problems; and (d) information on the status of grant-awarded projects, including whether any deferred projects (if any) for which the city was awarded grant funding have since lost those grants because of the city’s financial inability to move the projects forward.

4. The City Staff’s New Budget Plan Relies Heavily on One-Time Solutions

Last year, the city’s former Finance Director advised City Council that $3 million in ongoing budget solutions were needed in 2026-27 to effectively address the city’s funding gap. While staff advised that one-time solutions should be considered and adopted, it said permanent changes to city revenues and spending were needed to fix the city’s financial problems once and for all and halt the continued erosion, and ultimately, the depletion, of its General Fund reserve.

As noted above, the budget plan brought forward by city staff in its May 19 report contains a list of $1.4 million in expenditure reductions, many of which warrant serious council consideration and approval. However, most of these savings (about $1 million of the $1.4 million, by my count, based on their brief description on pages 06-5 through 06-7 of the May 19 staff report) appear to come from one-time budget solutions. The one-time savings appear to be these: Community Development, $200,000; Police Department, $90,000; Social Services and Housing, $200,000; Various, $500,000.

Moreover, as can be seen on pages 06-2, 06-8, and 06-21, the May 19 report, outlines a series of actions intended to increase the city’s General Fund reserve. The report briefly explains these as being “due to progress with outstanding audits, expenditure reductions identified by all departments, refinement of vacancy estimates, and staff analysis and clean-up of prior year encumbrances.” In addition, staff said, “Some of the major adjustments made since the mid-year report include: the transfer of State and Local Fiscal Recovery Funds (ARPA grant moneys) to the General Fund to reimburse for eligible expenditures, the recording of higher-than-expected investment income, and the correction of an entry that resulted in a decrease to General Fund expenditure projections of approximately $2 million.” The report does not provide a detailed explanation of these items, but all of the items mentioned appear to be one-time adjustments with no ongoing benefit in future years to the city’s fiscal condition.

These proposed solutions are substantial and will help to bolster the General Fund reserve in 2026-27 to $13.3 million, a 13.7 percent reserve. Because these are primarily one-time solutions, however, the city will need to take substantial additional budget actions just to replace these savings in 2027-28.

Accordingly, you should request that city staff: (a) verify which proposed budget reductions and technical budget adjustments identified in the May 19 report are one-timers and which will result in permanent ongoing savings; (b) identify any additional permanent savings solutions that city staff has considered but excluded from the May 19 report, their potential merit as budget solutions, and the reason for their exclusion; (c) provide a more detailed explanation of the nature of the various technical adjustments that increased the size of the General Fund budget reserve, including the fiscal impact of each specific measure it has scored as a budget adjustment; (d) explain how and to what extent errors in the recording of city fiscal transactions and other deficient operational practices resulted in the delayed discovery of some of these new funding resources, as well as to indicate what steps are and should be taken to better manage city finances to prevent their recurrence; (e) ask staff for their estimate of the General Fund gap the city will face in 2027-28, assuming that all of their proposals in the May 19 report were adopted.

5. Where is That New Fiscal Forecast They Promised?

As discussed above, many of the solutions offered in the May 19 budget package that would address the 2026-27 budget are one-timers that won’t help to address the ongoing structural budget shortfall the city will face in 2027-28 and beyond. This is not the approach that city staff had recommended last year. At that time they proposed the adoption of permanent ongoing budget solutions in 2025-26 and 2026-27 to solve the problem before the General Fund reserve erodes to a dangerously low level. Is the city facing a fiscal cliff in the next few years? Several weeks ago, city staff announced that the city was preparing an updated long-term General Fund fiscal forecast that would shed light on this question. However, that forecast, if it has in fact been prepared as promised, has not yet been released to the public, the Commission, or the Council.

That new forecast would shed light on the ongoing fiscal impacts of the budget solutions that are now being considered. But it would also clarify how changing economic conditions and decisions by other governmental agencies are affecting the city’s financial condition, for good and for bad. For example, an updated forecast would show the estimated full impact in the coming years of recent Council agreements with city labor groups on General Fund spending levels. The current uptick in inflation is likely to add to city costs by triggering larger automatic cost-of-living hikes in employee pay, which would be required under the terms of those labor deals, than the city had been assuming for future years. Those larger pay hikes would in turn automatically trigger larger than expected increases in city costs for employee pensions, vacation pay, and sick pay. All of that would ordinarily be reflected in that new fiscal forecast.

The new forecast could further indicate whether, and how much, inflationary increases in gasoline and other fuels could add to city operating costs. For example, increases in the price of gasoline and other consumer purchases could bolster city sales tax revenues. But a more shaky economy suffering from inflation could also depress the sales of automobiles, a major source of city sales tax revenue.

Accordingly, you should request that city staff immediately release an updated General Fund fiscal forecast so that information can be used to help guide the critical budget decision-making that is now occurring. The forecast should be used as the City Council intended, as a tool to guide and inform major city budget decisions, not merely as a way to record, after the fact, the fiscal impact of the budget decisions the city has made without the benefit of that information.

6. Surging Costs for Employee Pay and Benefits Will Likely Overwhelm New Budget Solutions

The significant increases in pay and benefits awarded to city labor groups in a series of labor agreements over the last few years, including two approved as recently as February, was ostensibly for the purpose of reducing city employee vacancy rates. The new May 19 budget report concedes that those huge payouts aren’t paying off. “The personnel vacancy factor used in the original adopted budget was approximately 4 percent of salaries and wages,” the May 19 budget report explains. “However, staff estimates that the average vacancy rate for the City has consistently been higher than 8 percent since 2024. Therefore, staff is proposing to revise the vacancy factor to 5 percent of total salaries and wages, which is still a conservative estimate of the impact of vacancies on the budget.”

That budgetary change will allow the budget to modestly reduce the amount of money the city will budget for its employees in 2026-27 and beyond. But those savings pale in comparison to the surge in employee compensation costs for pay and benefits the city is already experiencing and are about to get much worse for taxpayers. They are winning big. Page 06-20 of the May 19 budget report shows that, since 2022-23, the citywide costs of salaries and benefits for city workers (all workers, not just those like cops and firefighters paid from the General Fund), have increased about 27.7 percent, from $20 million a year to almost $94 million, since 2022-23. During that same four-year period, city revenues grew just 13.9 percent, as seen on page 06-18. The most recently available General Fund forecast demonstrates that the same pattern holds for employees supported from the General Fund. Nevertheless, in February, in the midst of an acknowledged budget crisis, city leaders unwisely signed off on two more such city labor deals for Police Department employees.

The contracts are excessive. City leaders have been asserting that the increases in compensation they authorized in those various multi-year contracts would bring total compensation for our employees in line with the median compensation (all pay and benefits) that a survey showed were provided to other public employees with similar jobs in our region. However, our signed labor deals threw in big one-time bonuses that city staff decided not to count as compensation, even though such bonuses in some cases were given out year after year. Then, we increased employee compensation with direct salary hikes, but ignored the fact that the city budget was also being increased to cover increases in premiums averaging 8 percent for health insurance for those same city workers.

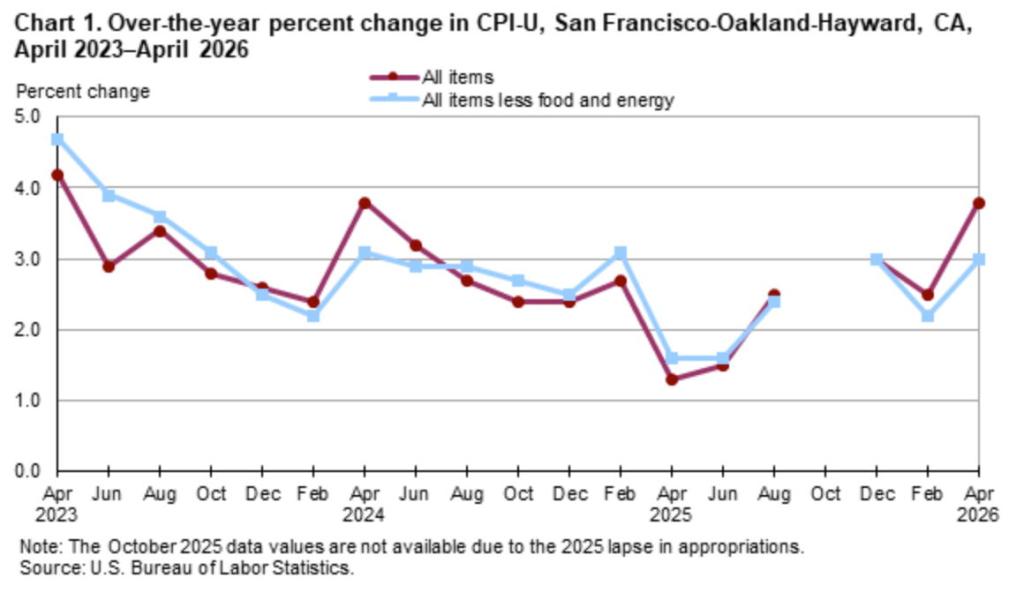

As a result, the City of Davis is exceeding the median compensation levels paid to other comparable city workers in our region. Then, in a move that creates additional fiscal pressure, city leaders essentially agreed to lock these excessive compensation levels with multi-year contracts. That means we won’t be doing year by year comparisons with other cities and adjusting our excessive compensation levels downward. Instead, our workers are now entitled to automatic cost-of-living increases in their pay each year. The increase in their pay will be based on an annual federal inflation index for the San Francisco Bay Area published each February. The February 2026 index increase will trigger 2.5 percent COLAs for many City of Davis workers. Due to the surge in gas and food prices caused by the war in Iran, the next COLA will probably be 4 percent, an increase much greater in its financial impact on the City of Davis than the one assumed in the most recent city General Fund forecast. The ominous inflationary trend can be seen in the chart below.

California health care experts predict that the continuing surge in health care premium costs for cities will continue, due in part to medical claims for more expensive drugs and therapies for the active and retired workers. Another factor increasing costs is last year’s federal cutbacks on public health care programs that will shift costs to other medical payers, including cities like Davis. The new city labor deals have included no changes that would have reduced those employee costs or offset them by sharing those costs with its employees.

The increase in pay from the COLAs automatically and directly impacts future city taxpayer costs for employee paid vacation and sick pay and pensions, and could easily overwhelm the value of any budget solutions the city adopts. Unfortunately, the City of Davis, which is smaller than most of the cities to which it compares itself, does not generate median levels of property or sales tax revenues to pay not just median compensation, but above-median compensation. Unless those excessive contracts are renegotiated, deep and painful cuts to city services our citizens enjoy are inevitable.

Accordingly, the Council should convene in closed session and immediately direct city staff to notify all city bargaining groups of its intent to negotiate changes to its current employee labor contracts to suspend COLAs for one year and to seek employee contributions to help offset the surge in city costs for health care for current and retired city employees.

Thank you for considering these important issues for Davis taxpayers.

Dan Carson

Leave a comment